Retirement Planning

Managing risk in retirement

Our retirement years come with several financial risks, but fortunately, you can take measures to help defend against each one. Many of these measures begin well before retirement.

Here are some more common financial risks, along with strategies to reduce each one.

Longevity

Canadians are living longer, but increasing longevity poses a risk – a retiree outliving their mutual fund savings. Today, retirees may need income to last 20, 25 or even 30 years.

Safeguarding against this risk begins with determining your retirement savings goal. You can find all kinds of calculators online, but we take a detailed and customized approach to arrive at a goal and retirement date you can regard with confidence.

During retirement, various methods are available to help your savings last your lifetime. A couple may split their pension income to pay less tax. A retiree may defer government benefits to receive higher payments at older ages. A risk-averse individual might purchase an annuity for a steady stream of income for life. These are just a few of the many strategies to help ensure you won’t worry about outliving your savings.

Inflation

Not too long ago, in June of 2022, inflation in Canada reached a 40-year high of 8.1%. Canadians may feel comforted that inflation is now around the Bank of Canada’s 2% target range, but mutual fund investors shouldn’t be lulled into a false sense of security. Even a 2% inflation rate can have a significant impact on your investments. That’s why inflation is sometimes called the silent thief of retirement savings.

Helping to control this risk involves two measures. First, the effect of inflation is taken into account when determining your retirement savings goal. Second, investments – especially low-risk investments – should offer yield or growth that aims to outpace the inflation rate.

Market volatility

Before retirement, market downturns can be mutual fund buying opportunities, but there’s no such silver lining during retirement if you’re not investing new money.

How does a retiree deal with market volatility if they still want some growth in their portfolio? One factor involves the time horizon. A retiree may feel comfortable holding equity funds in the earlier years of retirement, knowing the markets have time to recover in the event of a downturn. However, as the years progress, any retiree’s portfolio is typically adjusted to become more conservative.

Some retirees use a cash reserve to safeguard against market volatility. In a year when equity investments lose value, they draw retirement income from a pool of low-risk investments, such as money market funds.

Very conservative investors can simply hold little or no equity investments, favouring fixed-income funds and guaranteed investments.

Long-term care

Long-term care can be expensive, whether you receive private care in your home or live in a long-term care residence. As Canadians live longer, the probability increases of developing a medical condition or illness requiring such care. Almost three in 10 Canadians aged 85 and older live in a long-term care facility.1

You can purchase long-term care insurance to help manage this risk or set aside funds before retirement. If you choose to self-insure, these mutual fund investments can become estate assets if not needed for long-term care.

1 Statistics Canada, A portrait of Canada’s growing population aged 85 and older from the 2021 Census, 2022

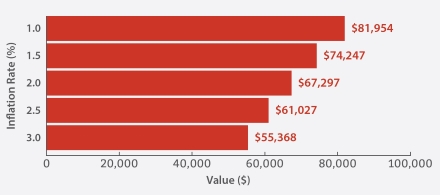

The impact of inflation

Purchasing power of $100,000 after 20 years

Even relatively low inflation rates have the potential to greatly diminish the purchasing power of savings. This chart is for illustrative purposes, showing the impact of inflation on savings that do not earn interest.

Source: Bank of Canada inflation calculator