Wealth Planning

Managing a millennial dilemma

Millennials are Canada’s largest generation, and many of them face a wealth planning dilemma. They want to start investing for retirement while they are younger to benefit from compound growth, but their current financial obligations make mutual fund investing a challenge.

Say that someone is saving for the down payment on their first home and worries about putting any extra dollars toward long-term goals. Or a couple with a home and a child want to save for retirement, but they’re making mortgage and car loan payments, paying insurance premiums, contributing to their child’s education, building an emergency fund and saving for a summer vacation.

Developing a plan

You solve the dilemma in three stages. First, you determine the amount you can commit each month or pay period toward your financial savings goals.

Second, list your current goals and categorize them by short-term, medium-term and long-term goals. Include important wants, not just needs. Estimate each goal’s total cost, and break down each one into how much to save annually and then monthly.

Third is the balancing act. You want to distribute your available savings toward meeting each objective, ensuring you can meet short-term and medium-term goals with mutual fund investments while staying on track to save for retirement and any other long-term goals. Also, you want to take care of your needs without sacrificing wants that are important to you. This stage usually requires some give and take. In some cases, you may want to look at tracking your expenses and budgeting to increase your amount of available savings.

With our assistance, you can also account for investment growth over time to help you reach each goal.

An evolving strategy

Your plan to meet multiple financial goals will evolve over time. Say you achieve a medium-term goal to renovate your kitchen. You might then dedicate your remaining savings toward one or more of your other existing goals.

Alternatively, a new goal may arise. Perhaps you want to help your child make a down payment on their first home. You might need to save more or make compromises to the amounts you allocate to other goals.

Certain life situations or events might also need to be factored in. For example, the financial challenges of a divorce may lead you to reassess your plan. Or perhaps a significant income increase may enable you to pursue your goals more aggressively.

We can work with you to adjust your plan as life events arise or your goals change. Also, we can regularly review the financial status of your goals to ensure you remain on track. This includes moving toward more conservative mutual funds for a specific goal as you approach the time when you need to access the funds.

More than financial

When you’re juggling multiple financial goals without a well-planned approach, you can become distressed. Having a strategic plan makes all the difference. Instead of feeling overwhelmed, you can be in control.

Over the years, when updates to your plan are required, you’ll be better able to handle the changes, having already experienced the goal-setting and give-and-take process.

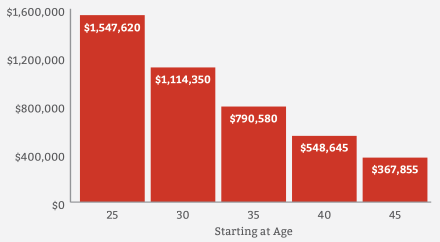

The advantage of starting early

RRSP value at age 65 with $10,000 contributed annually at 6%

Based on $10,000 contributed at the end of each year at an annualized interest rate of 6%, with interest compounded annually. This chart is for illustrative purposes only and is not intended to illustrate the performance of any security or portfolio.